Article: 4 Steps to get out of Debt

4 Steps to get out of Debt

You’ve finally made the decision. You are sick of every dollar leaving the second you get paid, the ridiculous fees and interest payments, feeling suffocated anytime you dare glance at your bank account, and living life too close to the edge at all times. You want freedom from feeling held down by your finances, from feeling trapped by your circumstances and from being a “slave to your lender”. You are ready to finally become Debt Free!

Now comes the real question, “How do I start my Debt Free Journey?”

This is one of the number #1 questions I receive and have seen asked across social media from people who are inspired by stories of debt freedom, but are crippled at the idea of tackling their own situation. Believe me, I have been there and I understand why you might feel overwhelmed. For most, this is uncharted territory. You may have never dreamed so big in your life, maybe you were never taught to. You might have been told that “people like us” will always have debt. Or maybe worse, taught that debt is a fact of life and more of a tool than it is bondage. You might not know anyone who is Debt Free or maybe you hadn’t even heard the concept till recently. Well let’s start here.

My name is Daniel, and my wife and I became debt free over 7 years ago and, more importantly, have remained that way since. Nice to meet you. Becoming and remaining Debt Free has been one of the most pivotal, life-changing actions I’ve ever taken and it has paid dividends in every corner of my family's life. After becoming Debt Free ourselves, we started to spark intrigue from friends, family members and acquaintances who had watched us along the way and wondered how we actually accomplished this feat. I have personally strategized with many of them to help them begin their own Debt Free Journey and have watched it literally transform entire family trajectories in the process!

So there you have it, you officially know someone who is Debt Free. You know what that means? There really is a chance for you!

Now to the point. How do you get started? I'm going to break down 4 steps you can take today to get you moving on your Debt Free Journey.

Let’s go.

Step 1: List Your Debts

First off, you need to get to know your debts. List them out and include the name, monthly required payment, interest rate and total balance owed. You may organize however you like, but we recommend ordering them from smallest to largest (total balance) to start.

Don’t know where to find your debts? Start by listing out the ones you know of and getting current numbers for everything listed above. Often times, these are easily accessible from lenders websites or with a simple phone call. If you aren’t sure where to even start, you can use a free Credit Monitoring app like Credit Sesame or Credit Karma to see what debts are outstanding and what your balances are. This will help you determine what’s out there so you can start defining each one.

Total your debts - Total the sum and the monthly required payment of all debts listed. This will give you your ‘become-debt-free’ number and help you understand how much money you can put toward your debt each month. Make sure not to put down the amount you’re paying as the minimum but the actual required minimum. Some of you might have just been throwing extra chunks of cash at random debts but we want to see the minimum so we can get after each debt with focus.

By the end of this step, you’ve listed all of your debts by name, have the total amount of debt owed, and know what your monthly obligation (required minimum payments total) is.

Step 2: Create a Monthly Budget

Your debts are listed, you know how much debt you owe in total and what your minimum monthly payments are. Now you're probably thinking "Great, but how am I going to actually pay all this off?" I know this moment can be daunting. This might be your first time actually seeing how much debt you have and you might think there is no way you can pay this off. I've totally been there. And the truth is that you can't keep doing what you've been doing and expect anything to change. It's gonna take new tools, new habits, new disciplines, and an attitude of hope and grit to get there.

This next step is a GAME CHANGER and will be one of the single most important tools you utilize on your Debt Free Journey and well beyond. A tool we have been using successfully for over 7 years! 💪

Many of you have probably had some form of a budget before. Maybe it went well, maybe you dreaded it. I get it, budgets can feel complicated and really tough to stick with. It takes discipline and practice to keep accountable to your budget so give yourself some grace and don’t overcomplicate it to get started. An 80% correct budget that you are actually using is much better than a 100% perfectly planned budget that never gets completed. But before I get too far ahead of myself, let's start at the beginning.

What is a budget?

For our context, a budget is a designated plan of your income, expenses and goals for a set period of time (a month in our case). You setup a budget so you can have a plan for your money in the month ahead rather than being surprised every time something happens. Your budget will not only give you a realistic plan for the month ahead, but set the bar for your spending habits and provide a tool for accountability when you overspend.

Where do I create a budget? For years people have kept a handwritten budget or used an excel spreadsheet. While these methods work for some (I'm a complete spreadsheet nerd, I'll admit, but don't use one for my monthly budget.) I would recommend finding an app to use on your smartphone or computer. While there are dozens to choose from the three that I like best are Every Dollar, YNAB, and Mint. Each of these have a free version (that is a great place to get started) and a paid version that comes with more features (bank connectivity being a big one.)

How do I setup my first budget? While most budgeting apps will give you a "sample budget" to get you started, every person's budget is going to look different depending on the unique factors of their life. Single? Married? In school? One Income? Irregular Income? Military? Contractor? The list goes on and on. Don't obsess over getting your first budget perfect. It's like a living organism. It will need to adapt from month to month and as your life changes. The key is to get started and get in a rhythm of using this tool regularly. You will have mistakes along the way and you will find certain categories not working for you. It's totally okay though, just adapt your budget and consider it for the next month.

While you are getting out of debt, the 4 basic categories for a budget are Income, Expenses, Debts and Saving.

Income - Plan what income you will receive and when you expect it. This includes paychecks, commissions, tips, side hustles, selling things around the house, and anything else that will provide income in the coming month.

Expenses - Expenses tend to vary month to month more than income. This category includes rent/mortgage, utilities, food, transportation, subscriptions, insurance, clothing, gifts, entertainment etc. The list should be inclusive of any expenses you know you will have in the coming month. There is a balance to laying out these categories. You don't want it so vague that you can't pinpoint spending issues or so specific that it's confusing and wastes time needlessly.

Example: You could easily have a single "Food" category that contains all transactions related to food (groceries, restaurants, going out with friends, coffee, food at work, entertainment, your morning coffees, etc.) But it wouldn't be specific enough to really show if you were spending $200 a month on Starbucks or eating out too much, would it? On the flipside, having twenty-four "Food" categories to capture the nuance of all the ways you consume food and beverages is probably overkill and will make tracking each transaction quite cumbersome . A balanced approach to this category might include "Groceries, Fast Food, Restaurants, and Coffee" or something similar to that. You decide what makes sense for you, just ensure it's accurate and easy to execute each month!

Debts - Since you are focusing on paying off your debts, you should have a separate section to track them. To start, this would just include your minimum monthly payments for each debt (listed in Step 1), but in time it will reflect the extra month you pay toward your debts each month. Don't worry, we will get to this in the next step.

Saving - This might be sparse as you are getting out of debt, but this is where you may plan for giving, upcoming expenses (like trips or owing on your taxes), or even saving for your first Emergency Fund.

Once you've created your budget, you should know if you have a surplus of money to put toward paying down debt each month (this is the goal!), or if you have a deficit each month.

For those of you that have a deficit, a question I get often is, "how can I pay down debt if my expenses each month are more than my income?" The simple answer is that you can't. If this is case for you, it's time to go back and revise your budget. You need to determine where you can cut expenses and/or generate more income. Easier said that done, I know, but this is the only way you can begin making strides toward becoming Debt Free. By actually putting money toward your debt each month.

Once you've created a budget that is accurate and has some level of surplus to pay toward debt, you are ready for the next step. There's a bit more work to complete, but this is where things get really exciting. By the end of the next step you will have a plan of attack for paying off your debt and a target date for when you will be Debt Free.

Step 3: Make a Plan

Alright, you've listed your debts and made a monthly budget. Way to go! You are on your way to beginning your Debt Free Journey and getting after your debts with intensity. But before you do that, you need to make sure you're seeing the full picture of your finances.

Your budget shows you your inputs and outputs for the month, but what if something unexpected happens? It's important that before you start to attack your debt, you have a buffer so when the unexpected hits, you don't return to old habits and create new debt to solve your newfound problem.

And what about assets? You know, savings, cash, investments, or things you own (even if they have debt against) that have value to them. What should you do with them?

This next step is where the whole picture comes together. It's where we make your roadmap to becoming Debt Free and an action plan of just how you will get it done. Let's dive in.

PART 1: BUILDING AN EMERGENCY FUND

Determine your Assets - An asset is any item of value that you own. This might be a car, a home, cash on hand, cash in a savings account, bonds, stocks or other investments, or any items of value that are in your possession.

Similar to your debts, we are going to list out all of your assets. You can determine how specific you want to be here, but I would keep it simple for now (think big items, not that binder full of Pokemon cards in the attic that “might be worth something now”.) The goal here is to see what you already own that might be helpful in getting some quick momentum on your Debt Free Journey.

Build an Emergency Fund - One of the most important things to do before you start crushing debt, is to make sure you have enough of a buffer to keep you from creating any new debt. For many, the first place they turn at any small sight of an emergency is their credit card. Need new tires? Credit Card. Can’t pay that bill? Credit Card. Don’t want to say no to happy hour with friends? Credit Card. Need to go school shopping for the kids? Credit Card. If you want to get out of debt for good. THIS MUST STOP NOW. You cannot expect to get out of debt for good if you keep turning to it every time you get in trouble. You need to learn the word NO first and foremost, then be adamant about sticking to your budget, and lastly have a non-debt solution for when small emergencies come (and they will. It’s a fact of life). This is where your Emergency Fund comes in!

How much should I start with? Some experts recommend $1,000 others recommend having 1-3 months of expenses. This is gonna look completely different based on your lifestyle circumstances, but I would recommend starting with around 1 month of necessary expenses. For a kid just out of college this might be $1,500 for a family of 4 in San Jose it might be $10,000. Ultimately this needs to be a small amount that you can save really quickly (think 1-2 months) in order to keep you from sliding back into debt while you’re trying to get out.

How do I come up with this? This is where your assets and budget come in. For some, you might already have some money in your checking or savings account that you can allocate toward this. Or maybe you need to sell some assets to create some cash. If not in assets, you might have a surplus in your budget and you can cash flow this amount in a short period of time. If so, great! Go with that and get your Emergency Fund built.

For others, you may have very little to your name and the thought of saving $1,500 seems impossible. It might be time to get scrappy. What do you own that you can sell on Facebook Marketplace or Craigslist? Maybe your credit card debt is from your love of shopping and it's time to sell some of your clothes on Poshmark or eBay? Can you get any overtime hours at work? Do you have any side hustle opportunities? Can you drive for Lyft, Uber Eats, or Door Dash? This is where you need to spark some creativity to figure out how to generate the income needed to build a buffer so you can start attacking your debt.

This Emergency Fund is just to get you started. Once you're out of Debt you can build a healthier emergency Fund of 6 months or even a year if you desire. But for now, this solely exists to keep you protected from minor emergencies and help you to not create any new debt.

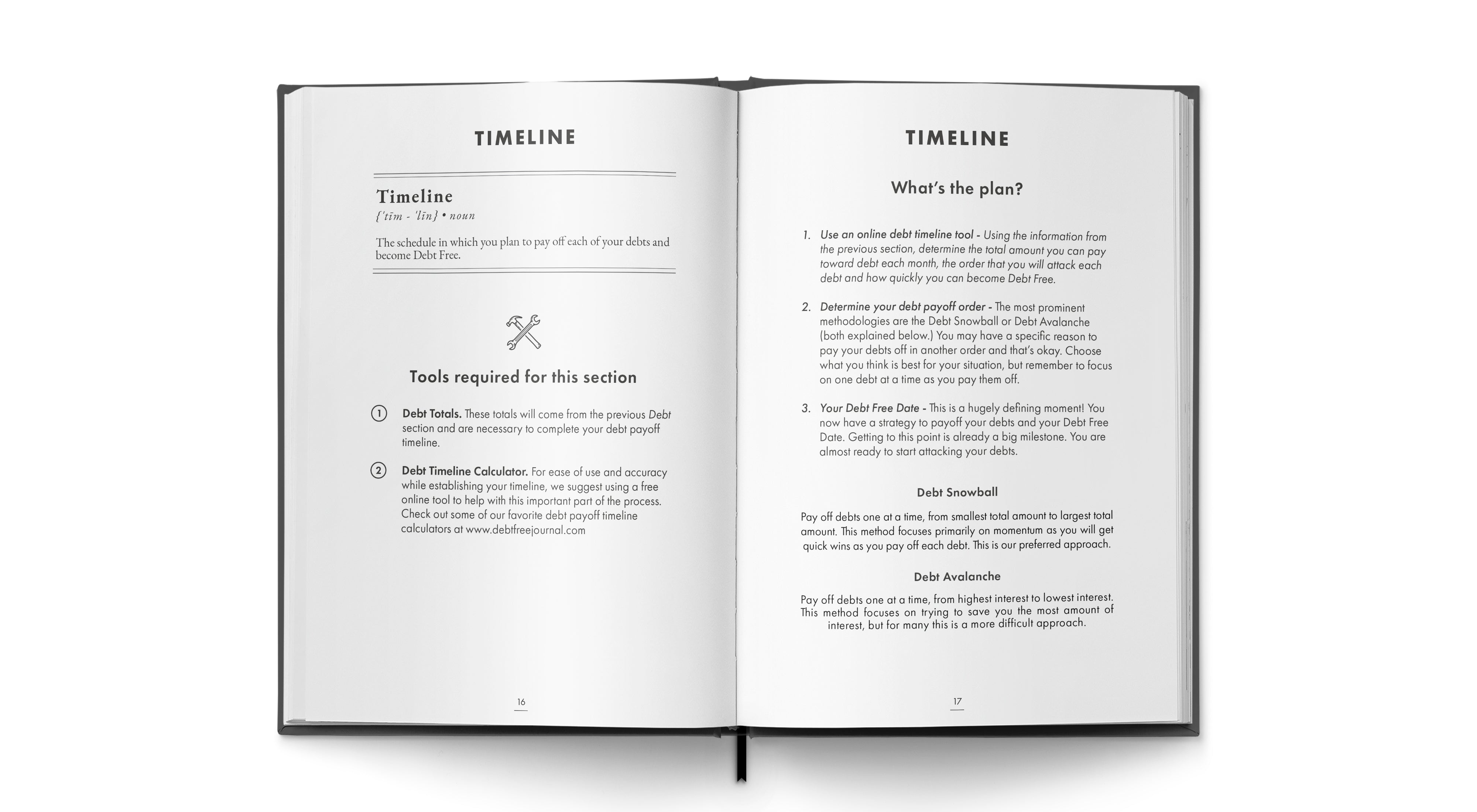

PART 2: DEBT TIMELINE

Now comes the debt. How are we going to get after this debt?! Well, you've listed all your debts, have a budget that tells you how much surplus you have each month, you've determined the size of your Emergency Fund and how you can fund it, and now we can actually start attacking the debts!

Determining your debt payoff order

Generally, I recommend the debt snowball method or debt avalanche method explained below.

Debt Snowball - Payoff debts one at a time, from smallest total amount to largest total amount. This method focuses primarily on momentum as you will get quick wins as you payoff each debt. This is our preferred approach.

Debt Avalanche - Payoff Debts one at a time, from highest interest to lowest interest. This method focuses on trying to save you the most amount on interest, but does for many is a more difficult approach.

You may have a specific reason to payoff in another order and that’s okay. Choose what you think is best for your situation. But remember to focus on paying off one debt at a time, only paying monthly minimums on the rest.

Debt Timeline

Now we get to the best part. Building the timeline for you to actually start paying off your debts! Using this amazing Debt Calculator, take the surplus amount from your budget, determine the total amount you can pay toward debt each month, how quickly you can become Debt Free, and the order that you will attack each. This will give you the order in which you will pay off your debts and target dates for when they will be paid if you stick to your plan.

In addition, this tool will actually provide your Debt Free Date. Your north star. The destination on the map. The big goal ahead of you. This is a hugely defining moment! You now have a vision and a plan to becoming Debt Free. You just gotta stick to the plan. Getting to this point is already a big milestone. I hope you're smiling 😁 even if it's a nervous smile

By the end of this step, you’ve listed your assets, determined your Emergency Fund amount, how to fund it, and when you will have it funded by. You've also created your Debt Free Timeline including the order you will payoff your debts, when each will be paid, and you Debt Free Date! Can you feel the momentum? Can you see hope on the horizon? Your Debt Free Journey is beginning and you know exactly where you are heading.

You are about to set off, there's just a few more things to say before you do.

Step 4: Pay Your Debts

You know your debts, you have a monthly budget, and you have a detailed plan of how to start attacking your debt. Now comes the hardest part, actually paying off your debts and sticking to the plan. For some this might be a matter of months, for others several years. No matter your circumstance, this is hard work that will stretch you, require self-control, patience, and discipline. You will fail along the way, but don’t worry, you aren’t alone! These small failures don’t define you, they are opportunities to learn and improve. Most of them will come from falling back into old habits, not saying no to yourself or others, or potentially from outside circumstances. When you fall, pick yourself back up, dust yourself off, and get moving again. If you stick with this plan and put in the work, you can become Debt Free.

Debt Free Timeline

Follow the timeline you built in Step 3 and start focusing your monthly surplus in your budget toward one paying one debt off at a time. With each debt you payoff you will build momentum and have more surplus in your budget each month to throw at the next debt. Keeping momentum is a huge part of moving toward your Debt Free Date and becoming Debt Free!

Motivation & Accountability

One of the main reasons people fail on their Debt Free Journey is they do it in secret. They have no support system, no one cheering them on, no one keeping them accountable, no one motivating them to stay the course. When my wife and I we’re getting out of debt, we struggled with all of these things and wish we had a more support from our community and better tools to keep us on track. This is where we can help! Here are a few things you can do now to help as you get started.

Share with trusted friends and family

Share your goals and journey with those you trust that are already your biggest cheerleaders in life. Tell them know why you are trying to become Debt Free. Through this process it's likely that a few people will really stick out as being your greatest encouragers and accountability partners.

Follow #debtfreecommunity & @debtfreecommunity on IG

There are over 1 Million posts in the #debtfreecommunity and we work to curate stories of hope, encouragement and empowerment on our page @debtfreecommunity. Follow both of these and other helpful accounts on social media to keep your goals in focus and be in an online community of like-minded people trying to achieve the same freedom you are.

Check out Debt Free Journal (20% Off for a limited time)

Confession, all of the information I just shared above is not original to this post...I borrowed all of it from Debt Free Journal.

Debt Free Journal is available right now at 20% off (with a freebie!) for a limited time. If the information in this post was helpful, please check it out and consider if it would be a helpful aid on your Debt Free Journey!

Above all, get started as soon as possible! The greatest thing that stops anyone from becoming Debt Free is inaction. Being so crippled about making the perfect decision that they don't make any decisions at all and give up before they even start. I hope this beginners guide has helped launched your journey and given you a foundation to build from and a roadmap for how to become Debt Free.

Here's to the journey,

Daniel

{kind=link}